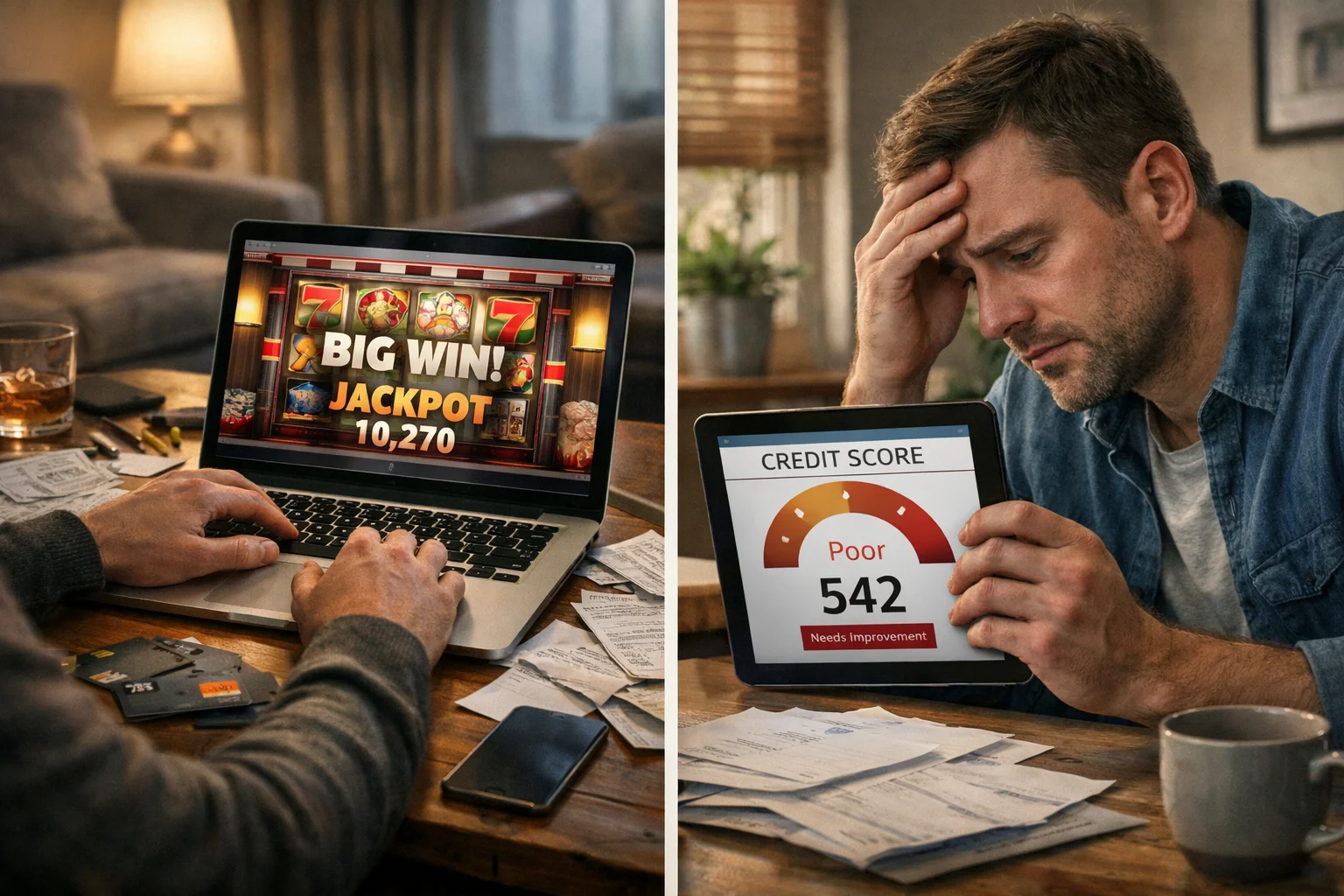

When it comes to gambling and credit scores in the UK, there’s a lot of confusion and misinformation. Many people assume that betting habits are directly visible to credit reference agencies, but the truth is more complex.

While gambling itself doesn’t directly impact your credit report, the financial behaviours associated with excessive gambling can have serious consequences for your credit health.

In this guide, we’ll separate the myths from the reality, helping UK consumers understand how gambling can influence creditworthiness both directly and indirectly.

Can Gambling Activity Be Seen on Your Credit Report?

Gambling transactions do not appear directly on your credit report in the UK. Credit reference agencies like Experian, Equifax, and TransUnion do not track what you spend your money on, only how you manage your credit accounts.

This means your visits to online betting sites or brick-and-mortar casinos are not recorded on your credit file.

However, it’s essential to recognise that although gambling isn’t itemised or highlighted within a credit report, the financial consequences of your gambling habits can be reflected in the data lenders see.

This creates an indirect connection between gambling behaviour and creditworthiness.

How UK Credit Reports Work?

Credit reports serve as a detailed financial footprint of your use and management of credit. They include information such as:

- Credit card and loan account balances and limits

- Monthly repayment history

- Number of missed or late payments

- Any defaults, County Court Judgments (CCJs), or insolvencies

- Credit applications and hard or soft searches

If gambling causes financial disruption that affects how you manage these accounts, it could still influence your score even if the activity itself remains hidden.

What Data Is Actually Tracked?

Credit reference agencies do not monitor individual purchases. Instead, they receive structured data from lenders and utility providers that include:

- Account type and status (active, closed, delinquent)

- Credit limit and outstanding balance

- Monthly payment performance

- Instances of missed or late payments

- Debt collection activity

So while your gambling expenditure isn’t shared, any credit behaviour resulting from gambling, such as unpaid bills or high debt balances, is captured.

Does Using Credit to Gamble Harm Your Score?

Using personal credit cards, overdrafts, or loans to fund gambling is a financial practice that can quickly deteriorate your credit health. This is especially true when gambling becomes frequent or problematic.

Many people don’t realise how easily gambling can inflate credit utilisation ratios or lead to borrowing practices that lenders interpret as risky.

High Credit Utilisation Explained

Credit utilisation refers to the percentage of your available credit that you’re currently using. Ideally, lenders like to see credit utilisation below 30 percent of your limit. Anything higher suggests over-reliance on credit and can drag down your score, especially if it remains high over time.

Here’s a practical example:

| Credit Card Limit | Outstanding Balance | Credit Utilisation | Risk Level |

| £1,500 | £400 | 26.6% | Low |

| £1,500 | £1,300 | 86.6% | High |

If you regularly use credit cards to place bets or deposit funds into gambling accounts, your credit utilisation can climb rapidly, even if you pay off part of the balance. Persistent high utilisation signals poor financial management.

Impact of Cash Advances for Gambling

Many gambling platforms accept deposits via credit cards, although this is increasingly restricted in the UK.

Some gamblers bypass this restriction by withdrawing cash from ATMs to fund gambling. This is known as a cash advance.

Cash advances are one of the most expensive forms of credit:

- They often incur a one-time fee of around 3 to 5 percent of the withdrawn amount

- Interest is charged from the day of the transaction with no grace period

- Rates for cash advances are usually higher than for regular purchases

These cash withdrawals will not reveal the purpose (i.e., gambling), but the transaction will show up as a cash advance.

Lenders tend to treat regular cash advances as a sign of financial strain, which can be damaging if observed during manual reviews.

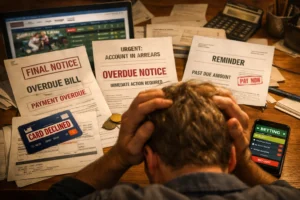

Do Missed Payments Due to Gambling Affect Credit Rating?

Missed or late payments are among the most damaging entries on a credit report. If gambling starts to interfere with your ability to manage monthly bills or debt obligations, it can leave a long-lasting footprint on your credit file.

When you miss a payment on:

- A credit card

- A personal loan

- A mobile phone contract

- A utility bill

…it is usually reported to credit reference agencies after 30 days. It remains visible on your report for up to six years, even if you later pay it off.

Gambling-related payment issues are often the result of one or more of the following:

- Prioritising bets over bills

- Chasing losses using credit

- Using future income to gamble

- Relying on short-term, high-interest loans

Once multiple missed payments accumulate, the risk of default increases. Defaults can have a serious impact on your credit score, often more than 300 points, and make future borrowing extremely difficult.

Can Lenders See Gambling on Your Bank Statements?

Although gambling does not appear in credit reports, many lenders—especially mortgage providers—request recent bank statements when you apply. This is where gambling activity becomes visible.

Banks and lenders often look at three to six months of your personal statements. What they are searching for is a pattern of behaviour, rather than a single transaction.

How Mortgage and Loan Lenders Assess Risk?

Lenders are trying to establish whether you are a financially responsible individual. Frequent gambling deposits, particularly if they are large or occurring near payday, can raise red flags.

Here are examples of what lenders may consider risky:

- Weekly betting transactions over £100

- Deposits made immediately after income credits

- Regular use of payday loans or overdrafts

- Bank balances falling to near-zero before month-end

This doesn’t mean all gamblers are denied credit. However, even if you have an acceptable credit score, excessive gambling behaviour on your statements may lead to:

- Reduced loan or mortgage offers

- Higher interest rates

- Additional scrutiny of your affordability

- Complete application rejection

Betting Patterns and Application Red Flags

If you gamble casually and manage your budget well, it’s unlikely to cause concern. But problematic betting patterns can give the impression of instability or emotional spending.

Some patterns that may lead to rejection:

- Spikes in gambling deposits during financial hardship

- High-frequency gambling over multiple platforms

- Evidence of bounced payments or declined transactions

- Gambling tied to loan deposit timings

Even when these patterns don’t lead to a poor credit score, they can harm your perceived affordability and reliability.

Does Gambling Affect Loan or Mortgage Approval in the UK?

Yes, gambling can influence whether you’re approved for a loan or mortgage, although it usually does so indirectly.

Many borrowers are surprised to find that their application is denied not because of a low credit score, but because of affordability assessments and the perceived risk linked to gambling.

Here are some core reasons why gambling affects approval:

- Lenders assess overall financial health, not just credit score

- Frequent gambling suggests unpredictable budgeting

- Deposits to betting sites may reduce disposable income

- Large or late-night transactions imply impulsivity

Lenders are bound by regulations to lend responsibly. If they see a pattern that could affect your ability to repay in future, they may decline the application even when other factors look good.

What Are the Long-Term Financial Risks of Problem Gambling?

For many, gambling is an occasional activity. But for others, it can escalate into a behavioural issue with long-lasting consequences.

The financial toll of problem gambling can become increasingly severe as individuals try to chase losses, cover debts, or juggle multiple credit sources.

Here’s a table outlining the indirect financial impacts of gambling on credit health:

| Behaviour | Potential Impact on Credit Score |

| Using credit for betting | Increased utilisation, lower score |

| Missed credit payments | Late payments reported to agencies |

| Payday loan use | Signals financial stress |

| Loan stacking | Higher debt-to-income ratio |

| Defaulting on bills | Default recorded on report for 6 years |

| Bankruptcy or IVA | Severe long-term credit damage |

These impacts don’t happen overnight but tend to build up over months or years of unmanaged gambling behaviour.

Can Responsible Gambling Still Affect Your Credit Score?

Even gamblers who consider themselves responsible need to understand the wider implications.

It’s not always the volume of gambling that matters, but how it interacts with your overall financial picture.

For instance, a person who earns £4,000 monthly and gambles £150 occasionally may not raise any concerns.

But someone earning £1,200 and gambling £300 every month may appear to be financially overstretched.

Responsible gambling still poses a risk when:

- It causes short-term cash flow issues

- You use credit products to extend play

- It delays important financial obligations

- It overlaps with other debt or financial stress

If these scenarios occur, they can influence how lenders assess your applications even when your credit score appears acceptable.

What Can You Do to Prevent Gambling from Hurting Your Credit?

Proactive financial planning and boundaries can help keep your gambling habits in check and protect your credit health.

Practical steps include:

- Use only surplus income for gambling activities

- Never borrow money to place bets or fund losses

- Set strict limits through bank settings or apps

- Monitor credit reports frequently via trusted agencies

- Schedule important bill payments first each month

If you’re concerned that gambling is beginning to affect your finances or your credit score, consider the following support options:

- Sign up for GAMSTOP to self-exclude from online gambling platforms

- Contact GamCare for confidential support

- Use StepChange for debt advice related to gambling

- Talk to your bank about transaction blocks for betting websites

Even if damage has been done, your credit score can recover over time. Most negative data ages out after six years, and rebuilding efforts such as making consistent payments and reducing debt can speed up recovery.

Conclusion

In the UK, gambling does not directly impact your credit score.

However, the financial consequences of gambling such as increased debt, missed payments, and poor financial behaviour, can seriously harm your credit rating and ability to secure future credit.

Lenders don’t judge whether you gamble they assess how well you manage your finances. By keeping your gambling habits responsible and avoiding credit-based funding, you can protect both your bank account and your credit reputation.

FAQs

Does gambling show up on a credit check?

No, gambling transactions do not appear on your credit report or in credit checks performed by lenders.

Can gambling affect a mortgage application in the UK?

Yes, lenders often review bank statements, and frequent gambling can flag you as a high-risk borrower, affecting your approval chances.

Is using a credit card for gambling a bad idea?

Yes, it can lead to high credit utilisation, fees from cash advances, and accumulating debt, all of which may damage your credit score.

Can I still get a loan if I gamble regularly?

Possibly, but lenders may consider you a higher risk, especially if your statements show consistent gambling or poor money management.

How long do gambling-related issues stay on my credit file?

Only the financial consequences like missed payments or defaults appear on your credit file, and these remain for up to six years.

What should I do if gambling has affected my credit score?

Focus on paying off debt, making payments on time, and getting help from debt charities or gambling support organisations to rebuild your score.

Can lenders deny credit just for seeing gambling on bank statements?

Yes, lenders can deny loans or mortgages if they see signs of irresponsible gambling, even if your credit score is acceptable.

![Top 20 Best Casino Apps for Safe and Fun Play [UKGC Licensed]](https://gaming.clickdo.co.uk/casino/wp-content/uploads/2025/10/Best-Casino-Apps-768x512.webp)